This morning’s key headlines from GenerationalDynamics.com

- Nationalistic tensions increase as UK and EU drift towards Brexit

- Japan’s government calls emergency meeting as yen surges after Brexit

- Israel and Turkey announcing a reconciliation agreement on Monday

Nationalistic tensions increase as UK and EU drift towards Brexit

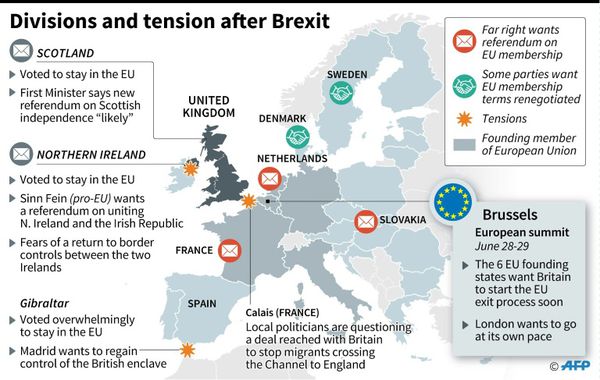

Nationalistic tensions grow in the UK and EU (AFP)

The successful Brexit referendum vote, calling for the United Kingdom of Great Britain and Northern Island to leave the European Union, has unleashed powerful nationalistic forces in both the UK and the EU, as we’ve been describing for years in nations around the world in a generational Crisis era. Furthermore, it has torn wide open new political fault lines within both the UK and EU, making resolution of the issues less likely and chaos more likely, and making both unions considerably weaker.

The latest developments are as follows:

- There is massive “buyer’s remorse” in the UK, with millions of people signing a petition for a do-over on the referendum. Everyone is saying that’s impossible, but one wonders if there’s an opening there.

- Jeremy Corbyn, the far left-wing leader of Britain’s opposition Labor party, who has previously been an opponent of the European Union, is being widely blamed by members of his own party for his half-hearted opposition to the Brexit referendum. Most labor unions want Britain to stay in the European Union, because they like the EU’s liberal labor laws. On Sunday, Corbyn’s leadership melted down, as twelve members of Corbyn’s “shadow cabinet” were pushed out or resigned, saying that they have no faith in Corbyn as a leader. (Since it’s possible for the British government to change hands overnight on a failing vote of confidence, an opposition leader will have a “shadow cabinet” that can immediately step in and become the real cabinet.)

- Prime minister David Cameron, leader of the “Tory” Conservative Party, who had strongly campaigned against Brexit said he would step down:

PRIME MINISTER DAVID CAMERON: The British people have made a very clear decision to take a different path. And as such, I think the country requires fresh leadership to take it in this direction. I will do everything I can as prime minister to steady the ship over the coming weeks and months, but I do not think it would be right for me to try to be the captain that steers our country to its next destination. This is not a decision I’ve taken lightly, but I do believe it’s in the national interest to have a period of stability and then the new leadership required. In my view, we should aim to have a new prime minister in place by the start of the Conservative Party Conference in October. And I will do everything I can to help. I love this country, and I feel honored to have served it. And I will do everything I can in future to help this great country succeed.

The impact of Cameron’s statement is that he will step down by October, and leave it to his successor to invoke the EU Lisbon Treaty Article 50, which starts the clock on the two-year process for Britain to leave the EU. Like the Labor party, the Conservative party is in chaos.

- What was unprecedented about the referendum is that the British people were badly split, but not along the usual Labor-Conservative lines. Instead, it was split geographically (England and Wales were pro-Brexit, Scotland and Northern Ireland were anti-Brexit), and it was split by generation ( “26-Jun-16 World View — Britain’s Millennials are furious at Boomers for Brexit vote”)

- It is pretty clear that the pro-Brexit leaders did not expect to win the referendum, and have no idea how to proceed next. Pro-Brexit leader Boris Johnson, who was on TV constantly before the vote, and who is the favorite to be the next prime minister, has been almost completely invisible since then, except to say that there’s no hurry in invoking Lisbon Treaty Article 50.

- This is driving EU leaders crazy, and stoking anti-British nationalism. Some of them are saying “Good riddance!” and want Britain not only to invoke Article 50 right away, but actually to leave the EU right away. Others are urging caution, and some are saying that even two years are not enough to figure out the terms of the divorce.

- Scotland officials are negotiating independently with EU leaders to figure out how Scotland can stay in the EU even when the UK leaves. There may be a new Scottish independence referendum.

David Cameron will be traveling to Brussels on Tuesday for a long-planned meeting of leaders of the 28 EU countries. But on Wednesday, he will be excluded from an all-day meeting of leaders of the other 27 EU countries, as they try to figure out what to do next. Guardian (London) and Democracy Now (London) and Breitbart News (London)

Japan’s government calls emergency meeting as yen surges after Brexit

The unexpected success of the Brexit referendum caught many investors by surprise, and has shocked the markets. ( “25-Jun-16 World View — Fallout from Brexit: Impact on geopolitics, economics, and stock markets”)

Investors quickly moved into “safe havens,” including dollar-denominated investments and, even more, into yen-denominated investments. This created a new global demand for yen, pushing the value of the currency higher, exacerbating Japan’s deflationary spiral.

The Bank of Japan and other government officials are holding an emergency meeting on Monday to evaluate the situation and to decide whether to “print money” and pour more liquidity into the banking system in order to prevent the vicious cycle that we described two days ago.

The European Central Bank would also like “print money” by buying bonds (quantitative easing), but according to one analyst, the ECB will have a problem doing this. The reason is that there are $8 trillion in bonds in the market at negative yields (interest rates), and the ECB is running out of bonds to buy. ( “15-Jun-16 World View — German 10 year bund yield goes negative, as deflationary spiral continues”)

The People’s Bank of China (PBOC) also announced a substantial weakening of the renminbi (yuan) currency, though they did it a different way. The yuan currency is pegged to a fixed exchange rate with the US dollar, and on Monday morning the PBOC weakened the yuan currency by 0.9%, its weakest fixing level since December 2010.

Meanwhile the favorite topic of all the tv financial talk shows has suddenly taken a dramatic twist. For months this year, these shows would debate for hours and hours each day whether the Fed would increase interest rates three times or two times or one time this year. Increasing interest rates would strengthen the US dollar, causing more deflation. So over the weekend sentiment has changed, and now analysts are expecting the Fed to lower interest rates, not raise them.

During the 1930s Great Depression, there was a “race to the bottom,” as countries kept devaluing their currencies in order to gain a competitive advantage against other countries. Ever since the “financial crisis” of 2007-8, it’s been widely feared that it could happen again, and the current situation is raising those concerns again. Dow Jones and Japan Today and Business Insider (Australia)

Israel and Turkey announcing a reconciliation agreement on Monday

Multiple media sources are saying that Israel and Turkey are announcing a reconciliation agreement on Monday, bringing to an end the deterioration in relations that followed the Mavi Marmara confrontation in 2010. (See “23-Jun-16 World View — Turkey drops lifting of Gaza blockade demand for normalization with Israel”)

According to press reports, the details of the agreement are as follows:

- Turkey had previously demanded that Israel eliminate the blockade of Gaza. The compromise is that Turkey will be allowed to transfer to the Gaza Strip humanitarian aid without limitation through the Ashdod port, and will be allowed to build both power and a desalination plants, and a hospital, inside Gaza.

- Israel had previously demanded that Turkey stop hosting Hamas officials in Turkey. The compromise is that Turkey will not allow Hamas to plan or carry out attacks against Israel from its territory.

- Turkey had previously demanded that Israel admit responsibility for the deaths of the Turks in the Mavi Marmara confrontation in 2010, apologize, and pay compensation to the families of the victims. The compromise is that Israel will not admit responsibility, but will apologize only for “operational mistakes.” Israel will pay $20 million to a special fund set up for the families, but this money will not be paid until Turkey’s parliament passes a law making it impossible for further Mavi Marmara claims to be made against Israeli officers or soldiers.

These have been difficult compromises for both sides.

According to a former minister to prime minister Benjamin Netanyahu:

Israel will pay Turkey reparations for the Marmara? I hope the reports are untrue. If they are true, this would be national humiliation and an invitation for further flotillas and libels by haters of Israel.

Turkish Foreign Minister Mevlüt ÇavuSoglu said the following:

Saying that Turkey has given up one of its two remaining conditions, which is lifting the embargo and blockade on Gaza, would mean humiliating the people’s intelligence. If Turkey had given up these [conditions], then relations would have been normalized by now.

The deal will be announced on Monday, and the agreement will be signed in July, according to reports. Jerusalem Post and Hurriyet (Ankara) and Al-Jazeera (Doha)

KEYS: Generational Dynamics, Britain, Brexit, European Union, Jeremy Corbyn, Labor Party, David Cameron, Tory, Conservative Party, Lisbon Treaty Article 50, Scotland, Northern Ireland, Boris Johnson, Bank of Japan, BOJ, yen, European Central Bank, ECB, People’s Bank of China, PBOC, yuan, renminbi, Israel, Turkey, Mavi Marmara, Gaza, Mevlüt ÇavuSoglu

Permanent web link to this article

Receive daily World View columns by e-mail

COMMENTS

Please let us know if you're having issues with commenting.