Standard & Poor’s rating service on Monday said that the bailout proposal by French banks (the so-called ‘French Model’) would prompt a “selective default” rating on Greek debt, according to Bloomberg, effectively sinking the plan. (We’re not talking about the 3-month bailout that we reported yesterday. We’re talking about the follow-on 120 billion euro bailout, to cover Greece’s debt payments through the end of 2013.)

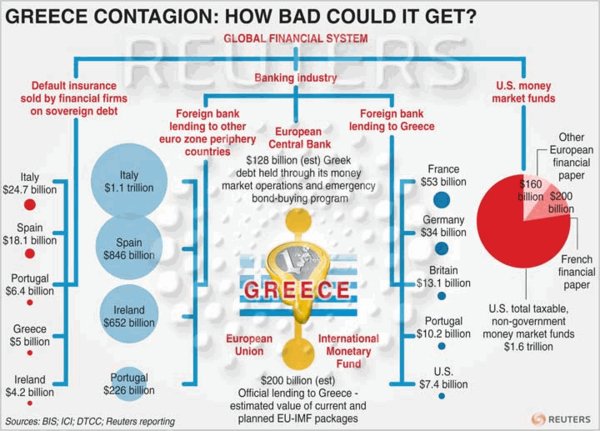

Exposure of various countries to a Greek debt default (Reuters)

Exposure of various countries to a Greek debt default (Reuters)

The S&P statement should hardly be a surprise to anyone. As I’ve written in the past, the assumptions of the French Model are inherently contradictory. The Europeans don’t want taxpayers to bear the entire cost of the bailout. So they want investors to share in the bailout. But they don’t want to force investors to share in the bailout, since that would force a default on Greece’s debt. So they want the sharing to be “voluntary.” But no investor would “voluntarily” lose money, so the whole idea is contradictory and impossible.

A European financial analyst that I heard on al-Jazeera on Monday said that the Europeans are absolutely furious that the S&P is torpedoing the European plan. “What right do Americans have to overrule the European government?” was being asked by unnamed European officials, along with unspecified threats against S&P.

None of the analysts I heard on any channel claimed that the rating statement was wrong. There was simply anger that S&P had told the truth. Thus, the unspecified threats amount to extortion to force S&P to commit fraud. Extortion and fraud are the norm today, especially in Europe.

S&P has good reason to be honest about its rating of the French Model. In the years up to 2007, Citibank, JP Morgan and other investment banks created and sold extremely complex CDOs and other synthetic securities that are mathematically provable as fraudulent. Nonetheless, S&P was bribed and extorted by the investment banks to give them AAA ratings, thus committing fraud. Extortion and fraud have been the norm for a number of years now.

But having committed fraud for so many years, and being blamed for a major part of the financial crisis, S&P now is not going to be too eager to commit fraud again, especially with the intense scrutiny going on today.

One of the most widely respected European analysts is Wolfgang Münchau, associate editor of the Financial Times. In a weekend column (Access), Münchau made a blistering attack on the French plan.

He accuses the European politicians of purposely making the French plan as complex as possible — as complex as a CDO — in order “to obfuscate facts and circumvent rules.” He summarizes the plan, and says:

“If this was any other field of human activity, you would go to jail if you accepted, let alone made such an indecent offer. …

All there is, is this dirty little con-trick. The complexity of the scheme is due to the need to persuade the rating agencies not to attach a default rating to Greek bonds.

The rollover agreement represents, from an economic point of view, nothing but a collateralised bond. It subordinates all other bondholders. The rating agencies would normally not hesitate to attach a default rating to Greek government debt.

So the solution is to create a complex structure, and claim that it is technically not a collateralised bond, but something that defies definition.

Just why the Greeks would want to accept such a ruinous deal is not clear to me. …

We have learnt from the financial crisis that one should not place too much faith in financial vehicles with three-letter acronyms. But that is what we are doing with this European equivalent of a late-period subprime mortgage CDO.

We are not just “kicking” any old “can down the road” any more. This is a can of explosives.”

Münchau wrote this column before the S&P downgrade, and as he suggested, “rating agencies [did] not hesitate to attach a default rating to Greek government debt.”

Greek privatization delusion

In order to get its 3-month bailout on Sunday, Greece’s parliament had to approve harsh austerity measures, including the privatization of state-owned companies on a massive scale, requiring employees of these companies to lose their jobs or to take substantial pay cuts.

Nobody believes that Greece will do this on their own, and so the EU is threatening to ‘massively limit’ Greece’s sovereignty, as we reported yesterday. The mechanism would be an external agency modeled on Germany’s ‘Treuhand agency’ that sold off 14,000 East German firms between 1990 and 1994.

It is delusional to think that Greece’s public sector labor unions will tolerate this without a great deal of violence. As one web site reader succinctly put it yesterday, “Greece will be happy to keep taking the money, but they have absolutely no desire (let alone ability) to pay any of it back. And if people think the Greeks are going to sit idly while Germany, the same people who invaded them during World War II, takes away their sovereignty from them, they’re delusional.”

The stakes are very high in Europe, and no one cares about anyone but himself. Fraud and extortion are the norm, and no one is safe.

An immovable object meets an irresistible force

On the one hand, you have the public sector labor unions, who are going to be asked to accept more and more job losses and salary cuts.

On the other hand, you have the donor countries – Germany, Finland, Slovakia and the Netherlands – who are going to be asked to give more and more to the debtor countries.

They’ll try to “kick the can down the road” as much as they can, but already they’re running out of options.

One of the great questions of philosophy is: What happens when an irresistible force meets an immovable object? We may be about to find out.

COMMENTS

Please let us know if you're having issues with commenting.