The Twilight Zone economy we are currently experiencing could implode if interest rates were to ever normalize.

Even mere whispers of this possibility can never be publicly acknowledged by any currently serving central banker; to do so would seriously undermine their legitimacy in the eyes of the public, who have become accustomed to their spoon-fed propaganda. These “experts” are the ones who are ultimately responsible for the problems we now face. They allow politicians to spend beyond their respective countries’ means, then give them blank checks to bail them out whenever they get into too much trouble.

Built upon an ever-increasing mountain of debt, any significant uptick in rates could bring the whole financial system down. Most existing borrowers, be they individuals or institutions, would likely be unable to handle higher payments if forced to refinance at pre-2008 levels.

Have you ever met a lender or real estate broker who tried to get you to spend LESS money?

How many of you reading this right now could make payments on a new 30-fixed rate home mortgage if rates rose from the current 3.6% to 5.0%? What if they increased to 6.0%, where they were in the summer of 2008?

On a much larger scale, from businesses and entire nations, the hard choice of living within one’s means has been rejected by short-sighted voters who seemingly aren’t doing the math or thinking of the implications beyond just a few years.

No one above an elementary school education can deny that it is mathematically impossible to pay down our current debt bubble with sound currency or without using questionable accounting methods. The world’s financial system has crossed the Rubicon in its ability to fix this problem without all future growth and productivity gains being consumed by interest rate expenses.

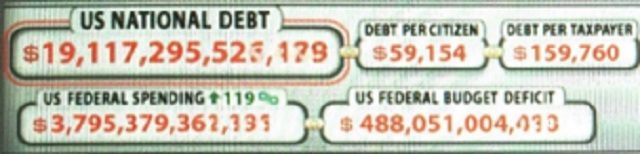

Look at the two charts below, taken from the U.S. Debt Clock, and note the debt per taxpayer sections (a 14x jump from 1980 to 2016). During this timeframe, income has failed to keep pace with the mounting debt.

March 16, 1980

March 16, 2016

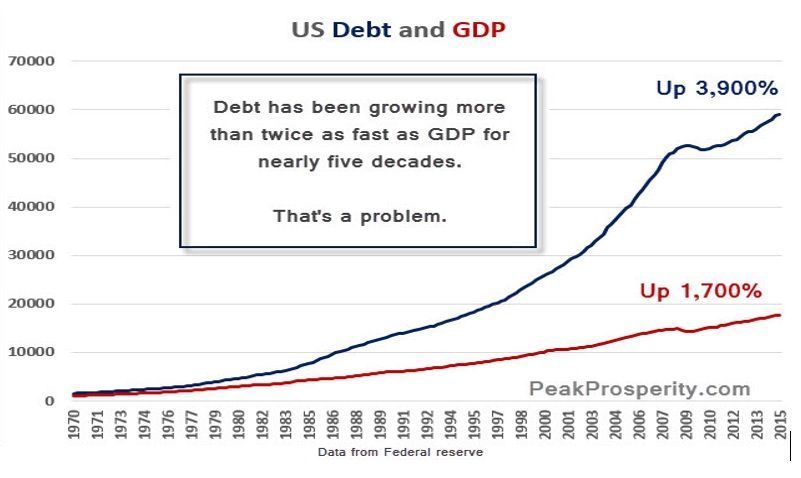

This next two chart show how the Keynesian shell game has worked since we adopted the fiat money system on August 15, 1971. Debt has grown at more than twice the rate of GDP. This is nothing short of a debt-based Ponzi scheme that has entered the terminal stages. Everything has its limits, even debt. The recent adoption of negative interest rates by over 20 advanced countries as some solution to this failure is akin to financial chemotherapy that will likely damage or kill, rather than provide the needed cure.

The economy would be in an official financial depression if not for the world’s central banks conspiring to push rates down—effectively stealing from savers. This policy is no different than cutting off your leg to feed yourself when on the brink of starvation—you may no longer be hungry, but you’ll still bleed out. When the Fed drops rates to benefit people purchasing and refinancing homes, for example, savers have to resort to eating into their principal. This one action is likely going to be the cause of the next mounting financial crisis: pension and insurance failures.

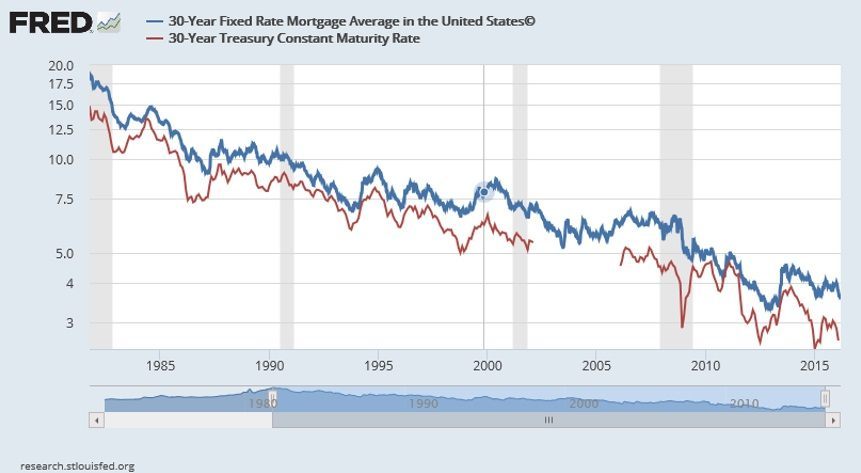

Since Home Mortgage rates peaked in October of 1981, the U.S. economy has experienced an unrelenting tailwind. This fall in interest costs has allowed everyone in the economy, from public to private, to borrow and refinance. This cycle, as depicted in the chart below, highlights just how far rates have fallen since October of 1981.

Rather than use the savings gained from the lower rates to pay down the principal on the debt, the opposite has occurred—it has encouraging even more reckless borrowing. The central bankers are playing with fire by allowing this debt to continue to expand. A day of reckoning is on the horizon; one which will likely start in Japan and be followed by Europe. These two economies are in the worst financial shape, hamstrung by falling birth rates and debt loads well above 100% of GDP.

But aren’t corporations doing well?

Corporate earnings are being propped up by rolling (refinancing) their debts into lower and lower rates, and borrowing to buy back outstanding shares. If a firm can purchase 10% of their outstanding stock, then earnings get a nice boost without them ever having to increase sales. This buyback strategy has buoyed some of the largest firms all over the world, as they are the ones able to borrow at the most favorable rates.

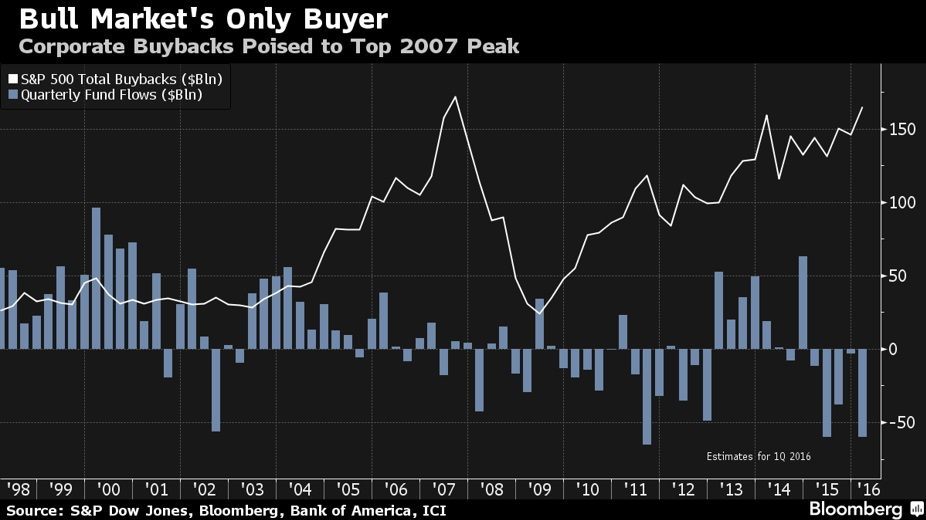

Looking at a real world example, one might wonder what might necessitate a company like Apple to borrow money. The most profitable publically traded company in the whole world, with a pristine balance sheet and billions in cash holdings, is borrowing money and buying back stock. This is NOT a recommendation on the purchase of Apple stock, but instead an observation about that nature of what low-interest rates do to pervert the capitalist system. Historically, firms once borrowed to invest in new equipment and R&D. Today, they are engaging in a buyback orgy that is significantly larger than equity purchases by institutions and retail investors.

The chart below shows how fund flows have been negative for five quarters now, and that even when they have been positive, they are dwarfed by corporate purchases. The largest buyers of stocks have been and continue to be corporations. This is what has been fueling the Fed’s “wealth effect” manipulations. This begs the question: What would happen if this buyback bonanza significantly slowed or stopped?

The solution to all of this is to stop the manipulation of interest rates and begin the painful reversal by beginning to live within ones means. Stagnation is the best we can hope for going forward. The longer this game of manipulating interest rates go on, the larger the future problems we will have to face. No one likes pain. No one likes change. Nevertheless, those days of whistling past the graveyard have passed. If we act now, the hope of living through this, rather than it crumbling all around us, increases exponentially. We must face reality and own up to our obligations by paying our debts. We must accept responsibility for our misguided collective mindset of choosing to have our cake and eat it too—the philosophy that has led us to this point and that we can no longer afford to indulge.

***Nothing in this article should be taken as an endorsement to buy or sell any security.

COMMENTS

Please let us know if you're having issues with commenting.