For much of the Biden presidency, the Main Stream Media-approved economic experts have been nonchalant about inflation.

Even as prices were rising—gasoline, for instance, jumped by about 20 percent in the first two months of the Biden presidency—the public was advised to stay calm.

Sample March 10 headline from the reliably pro-Biden New York Times: “Inflation Fear Lurks, Even as Officials Say Not to Worry.” The article quoted Jerome Powell, chairman of the Federal Reserve, saying that the price-spikes were nothing to be concerned about. According to Powell, “There’s a difference between a one-time surge in prices and ongoing inflation.” The Times explained that Powell “expected the coming increase to be transitory.”

The same article quoted Kathy Bostjancic of Oxford Economics saying, “Outside of another buoyant advance in energy prices in February, consumer price inflation remains very tame.” And the piece also quoted JP Morgan Chase CEO Jamie Dimon saying of inflation, “I wouldn’t worry too much about it.”

Yet then a funny thing happened: Inflation happened. On July 13, we learned that the Consumer Price Index rose 5.4 percent over the preceding year, and on July 14, we learned that the Producer Price Index surged 7.3 percent over the previous 12 months. At these rates, prices would double in the next 10 to 15 years. Or, to put that another way, the value of a dollar would be cut in half.

More recently, some of those, uh, experts have had a change of mind. For instance, Dimon said on July 14, “The inflation could be worse than people think.” He added, “I think it’ll be a little bit worse than what the Fed thinks. I don’t think it’s only temporary.” And on the 15th, Treasury Secretary Janet Yellen allowed, “I think we will have several more months of rapid inflation, so I’m not saying that this is a one-month phenomenon.” Still, she insisted that price increases will reach “normal levels” over time.

We are all free to wonder, of course, why we should now believe the same experts who were wrong in the past.

U.S. Secretary of Treasury Janet Yellen testifies during a Senate Appropriations Subcommittee hearing on June 23, 2021 in Washington, DC. (Shawn Thew-Pool/Getty Images)

In the meantime, Republicans, who had been warning about inflation ever since the Biden spending binge began, have been in full throttle, blaming inflation on Democratic spending and warning of more price-hikes. Said House Minority Leader Kevin McCarthy (R-CA), “This is a tax on every single American. It doesn’t matter what product you’re buying, it costs you more money. What government is doing, it’s creating inflation.” And speaking of the big $1.9 trillion Biden stimulus package enacted in March, McCarthy, thinking ahead to the next midterm election, recalled: “It was passed just along party line with only Democrats voting for it.”

Bob Luddy, writing for The American Spectator, laid out some of the numbers underlying the new inflation:

Government spending is ballooning our national debt, which already exceeds $28 trillion. The federal government has collected on average 17.4 percent of GDP in taxes over the past 50 years, including 16.3 percent of GDP in 2019, but it is currently spending well in excess of that, including 36 percent of GDP in 2019 and 44 percent of GDP in 2020.

But wait! There’s likely more spending coming: As Politico Playbook reported on July 15, Democrats are having a “love fest” over their new $3.5 trillion budget plan: “President Joe Biden received multiple standing ovations during a private lunch [in the Capitol] where not a single [Democratic] senator complained about the price tag.”

Indeed, speaking for the Democrats is Sen. Bernie Sanders, the democratic socialist from Vermont, also the chair of the Senate Budget Committee and the principal architect of the new plan. Asked about inflation on CNN, Sanders was mostly dismissive: “I am concerned about inflation, among many other things.” And he added, “As I think you know, this bill, this 3.5 trillion, and then there’s another 600 billion in a so-called bipartisan infrastructure bill, will pay for itself.”

So just as you might have expected, Sanders isn’t really worried about inflation; his mind is on other things.

Yet for others, a new conventional wisdom is settling in: Inflation is here to stay. Hence this July 14 headline from CNN: “Why inflation may not go away anytime soon.” (Now they tell us.)

Still, for his part, Fed Chairman Powell is still a believer in his non-inflation promises. As he said on the 14th, inflation “will likely remain elevated in coming months” before “moderating.”

Powell’s faith that inflation is not a problem drew a tart comment from Breitbart News’ John Carney:

In a heartening demonstration that hope springs eternal, Fed chair Jay Powell went before Congress today to say that despite the Consumer Price Index and Producer Price Index coming in much hotter than expected, he remains untroubled. Sure the Fed underestimated the power of the inflationary forces that the combination of zero interest rates, $120 billion a month in bond purchases, and a promise to ignore inflation would summon forth from our darkest path. But the public should “have faith,” as Powell put it, in the Fed’s ability to stomp down inflation if things get bad enough.

And of course, some Democrats, such as Rep. Alexandria Ocasio-Cortez of New York and Rep. Maxine Waters of California, insist that inflation is nothing to worry about.

Yet Republicans weren’t buying it, even as they were thinking back to previous eras of inflation.

Sen. Ted Cruz of Texas tweeted on July 13, “It’s like we’re reliving the worst part of the 70’s all over again.” Cruz, born in 1970, can have only childhood memories of that decade and yet in that decade, inflation was so severe that even for the young, bad memories of inflation were deeply etched.

We might consider: In 1970, the price of a gallon of gasoline was 36 cents, while in 1980 it was $1.19. In other words, the price of gas more than tripled. Even a kid would remember that.

Moreover, during the 1970s, a gallon of milk went from $1.32 to $2.16. And the median home price jumped from $24,000 to $58,000.

To consider inflation in a more precise statistical form, we can turn to the Labor Department’s Consumer Price Index (CPI). For its data-crunching purposes, the department takes the years 1982-84 as a baseline, assigning a baseline value of 100, and then it calculates prices before and since. By this measure, in 1970, the CPI stood at 38.8, which represented a 5.8 percent increase over 1969. A decade later, in 1980, the CPI stood at 82.4, which was a 13.5 percent increase over 1979.

In other words, during the ’70s the CPI more than doubled, from 38.8 to 82.5, as did the annual rate of inflation, from 5.8 to 13.5.

So what was the cause of this inflation? Most experts attribute it to the overheating of the economy due to the twin federal spending bulges of the late 1960s: the Vietnam War (an actual foreign war) and the War on Poverty (a surge in domestic spending). In other words, the U.S. was suffering from runaway Keynesianism, that being the economic doctrine that had guided the country since the 1930s.

What It Was Like Living With Inflation—and How It Was Ended

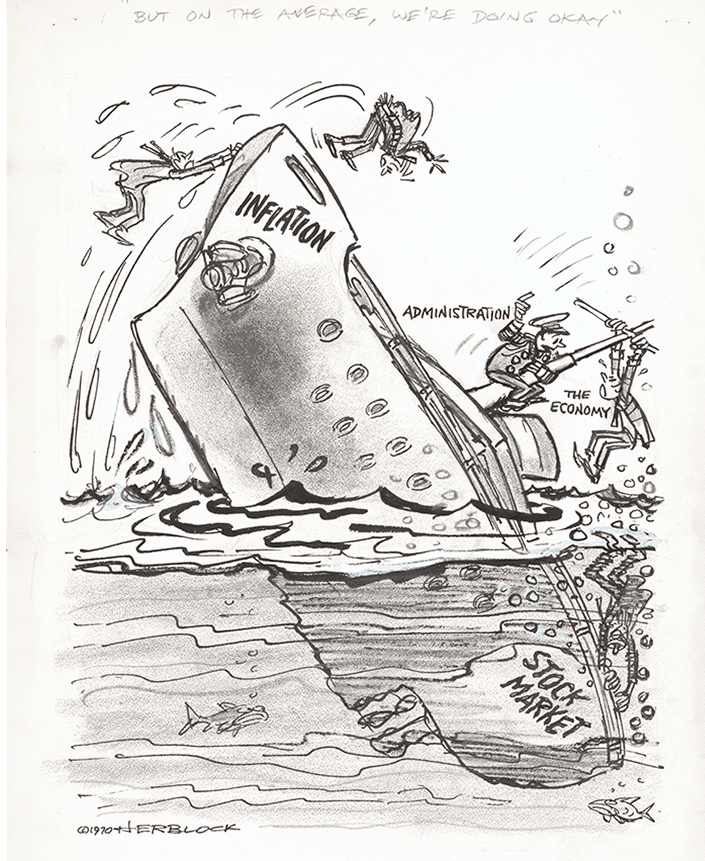

This Baby Boomer author well remembers the 1970s. During that decade, rising prices were a constant topic of discussion, often mentioned in political cartoons; for instance, one showed inflation as the shark from the 1975 movie Jaws, while another showed it sinking the economy altogether. And one poignant cartoon played on the impact of inflation on savings, draining away purchasing power: An older man, beset by high prices, says to his wife, “Here’s a bit of nostalgia for you. I’m saving exactly the same amount per week now as I did when I was in grade school.”

“But on the Average, We’re Doing Okay,” 1970. Published in the Washington Post, May 22, 1970. Graphite, India ink, and opaque white over graphite underdrawing. (Herbert L. Block Collection, Prints and Photographs Division, Library of Congress)

Popular unease over inflation soon led to a political response. In August 1971, President Richard Nixon imposed temporary wage-and-price controls. Over the next few years, these bureaucratic controls came in and out, applying to some sectors and not others. The predictable result was chaos. Soon the economy was suffering from shortages, as producers stopped producing in the face of too-low prices. Back then, legendary TV comedian and host Johnny Carson was using his nightly 90 minutes to joke about shortages.

Moreover, as inflation compounded with price controls to produce economic inefficiency, even sectoral breakdowns—such as the epic gasoline lines of 1973-4 and 1979—the result was stagnation, as well as inflation, which came to be known as stagflation.

In this Dec. 23, 1973, photo, cars line up in two directions at a gas station in New York City. Of all the bad memories seared into the American consciousness from the early 1970s, the never-ending lines at the gas pump has to top the list. (AP Photo/Marty Lederhandler)

Stagflation led to a national funk. Back then, another unfortunate oft-heard word was “malaise,” which the White House of President Jimmy Carter used on itself in 1979. And as another political cartoon had it, inflation and recession were two wild horses, galloping together.

During that bleak decade, books on the topic of inflation became important conversation pieces; indeed, socioeconomic thinking turned dark, as long-memoried observers recalled the catastrophic hyperinflation of Germany in the 1920s, which helped pave the way for Hitler to come to power in 1933. (Interestingly enough, the centennial of the onset of that ill-starred hyperinflation came this past June.)

So what happened to the Great Inflation of the 1970s, which spilled over into 1980, the last full year of Jimmy Carter’s presidency? In that year, a new president, Ronald Reagan, was elected, defeating Carter by a wide margin. Then inflation, having peaked at 13.5 percent under Carter, fell dramatically under Reagan, bottoming out at a tiny 1.9 percent.

President Jimmy Carter dropped by a meeting of business leaders in Washington on March 29, 1979, asking their help in controlling inflation. From left: Willis Alexander, vice president of the American Bankers Association, center; Carter; and Tom Murphy, a General Motors Company executive. (AP Photo/Dennis Cook)

We might ask: After a decade of bad news about inflation, why the good news? One positive factor was the tight-money policy of Federal Reserve Chairman Paul Volcker, who was appointed to the post by a desperate Carter in 1979 and then reappointed by Reagan in 1983.

Yet another factor, too, was the opening up of the economy. And what do we mean by that? We mean that if we start with the standard definition of inflation—“too many dollars chasing too few goods”—then we can see that there are two ways to reduce price-rise pressures: first, contract the supply of dollars (which happened under Volcker’s Fed); and second, expand or open up the supply of goods.

As liberal writer Michael Tomasky–who laments, of course, the rise of Reagan—conceded in the New York Times two years ago, “Inflation was Keynesianism’s Achilles’ heel, and the supply-siders aimed their arrow right at it.”

So that’s what Reagan did bigly: he expanded supply. His guiding policy idea after all—inspired by Rep. Jack Kemp (R-NY), economist Arthur Laffer, and polemicist Jude Wanniski—was known as supply-side economics. (Reagan was further inspired, of course, by the larger school of free-market economists, from Adam Smith to Milton Friedman.)

In office, the 40th president enacted a bold agenda of supply-side policies. These included, of course, tax-rate cuts, and yet they also included additional spending for tech, as well as deregulation that helped along something that would become known as the Internet.

Thus in so many ways, Reagan enlarged the economy’s supply side; that is, the dollars were chasing more goods not fewer, and so inflationary pressures eased.

And so that’s how Reagan defeated stagflation; he tightened money and loosened supply. Thus the Gipper’s economic success speaks for itself: Even as inflation fell, unemployment fell too, and the economy grew by a third.

Ronald Reagan emphasizes a point with his finger during a speech at the World Congress Center in Atlanta on Nov. 16, 1979. Reagan said President Carter has turned inflation and energy into national disasters and says the problems can be solved if he is elected president. (AP Photo)

So now to today. Maybe once again we need supply-side expansion. However, it doesn’t appear that President Joe Biden agrees. Yes, as a young senator from a swing state, Biden shrewdly voted for Reaganomics in the ’80s, and yet as president four decades later, one of his first moves was to shut down the Keystone Pipeline, even as his administration took additional steps to stymie energy supplies. So it’s no wonder that gas prices have gone up, just as they did in the ’70s.

More broadly, by reversing the Reagan formula, Biden seems happy to constrict the supply side with new taxes and regulation, even as he cranks up the demand side with more spending. So inflation is already here, and stagflation looms dead ahead. (In fact, here at Breitbart News, this author has chronicled the many ways in which Biden seems determined, or at least destined, to repeat Jimmy Carter’s policies.)

To be sure, many MSM-approved experts are still saying that Biden is doing fine. And yet a few surviving Baby Boomer liberals today are sounding the alarm, warning younger liberals–who have no memory of the Great Inflation of the ’70s, and not enough book-learning, obviously–about the tidal wave to come.

One such warning voice comes from Ed Kilgore; writing in New York magazine, he called inflation “poison for progressive politics.” And another warner is Timothy Noah; in the pages of The New Republic, he declared, “Inflation is death to progressive governance because it makes people feel that the government is spinning madly out of control.”

Interestingly, both writers took on a notably resigned tone; that is, neither seemed optimistic that the youngsters were going to heed the advice of their elders. We can observe: As with so many things, every new generation seems to think that the old rules apply only to geezers; for the young, This time it’s different. And this is how each generation usually learns the hard way.

Yet in the meantime, over the next few years, the broad mass of voters–the folks that Kilgore and Noah are worried about–will get a say. And if history is a guide (and it is), the folks won’t like stagflation.

In fact, instinctively, many voters will be looking to the supply-side, thinking about not only tax cuts and more energy as a source of growth, but also about other supply-expanding policies. For instance, there’s Operation Warp Speed, which lights a beacon on the path toward the fast-track production of innovative medicines. And there’s space tourism, which could be the launchpad for a host of new space ventures and industries. These and other tech breakthroughs would increase supply, and thus would help hold down prices.

Yet in the short run, as we look for historical precedents to inform our political thinking, we might look back to the political capper on the 1970s, which was the 1980 election. In that year, Jimmy Carter’s demand-side pessimism was pitched against Reagan’s supply-side optimism.

Reagan won that election in a landslide, and that victory provides a promising template for 2024.

COMMENTS

Please let us know if you're having issues with commenting.