November Jobs Rain on the March Rate Cut Parade

The November jobs numbers were a kick in the teeth to traders betting that the Federal Reserve would start cutting rates in March.

The economy added 199,000 jobs on a seasonally adjusted basis in November, a big jump from the 150,000 for October. This was stronger than expected. What’s more, the unemployment rate moved back down to 3.7 percent from 3.9 percent, which no one had in their forecast.

The effect of this has been to destroy the narrative that the labor market was on a glide path to looser conditions. That narrative never made much sense since we really only had one month—October—of anything that really looked like a significant softening in the labor market. When monthly data happens to fit the prevailing wisdom, the market often forgets the rule that you should not make too much of one month’s data.

It was only two weeks ago that the market was assigning a 70 percent chance that the Fed would cut rates at the March meeting. That was maniacal market excess. Fed officials have made it very clear they look to things like three- and six-month averages rather than month-to-month data. There was never a very good chance—barring some unforeseen geopolitical catastrophe—that the averages for employment or inflation would have fallen far enough to justify a cut in March, much less a 70 percent chance.

Even as late as yesterday, the odds of a cut were better than even. The jobs numbers on Friday flipped the odds to favor the Fed holding steady through the March meeting. Even at around 44 percent, where they stood at lunch time on Friday, the odds implied by the fed funds futures market seem out-of-whack with reality. It’s not that a Fed cut in March is impossible, but it remains extraordinarily unlikely.

‘Tis the Season…for Misleading Seasonal Adjustments

It’s worth noting that the October slowdown in job growth that birthed so many early rate cut hopes was entirely an artifact of seasonal adjustment. Before seasonal adjustments, employers added more than one million people to payrolls, making October the second strongest month for hiring all year after February (which, by the way, was also reported as a slowdown in hiring on a seasonally adjusted basis).

There’s good reason the government releases seasonally adjusted figures. When you are trying to assess the underlying strength of the labor market and the direction of employment, it can be helpful to smooth out seasonal volatility.

That’s not reason to ignore the unadjusted figures. For one thing, the unadjusted figures are what people are actually experiencing in their lives. Households do not feel better or worse about the economy because of seasonally adjusted figures, whether that is employment, inflation, or consumption. It’s the unadjusted figures that matter on a practical level.

The Secret Growth of Retail Jobs

The danger of ignoring the unadjusted jobs figures was highlighted by the furrowed brows over the Labor Department’s report that retail employment had fallen in November. Shouldn’t retail employment rise as we come into the holiday season? Could this be a sign that the long-resilient consumer was finally buckling under pressure from the Fed’s interest rate hikes?

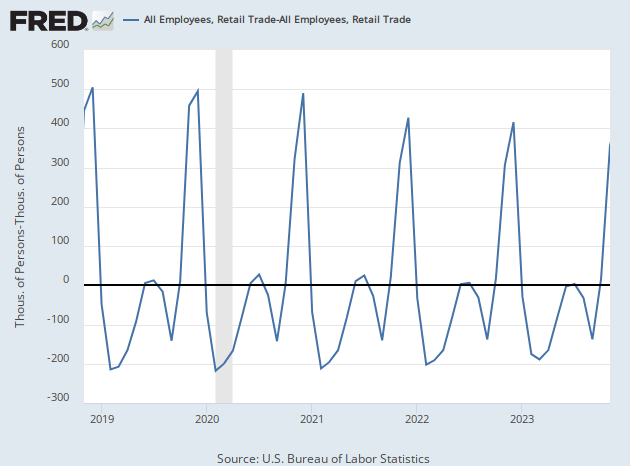

The seasonally adjusted number showed retail trade contracted by 38,400 in November. Before adjustment, however, retail trade added 264,200 jobs. Employment in retail did rise in November, by a lot. It just did not rise by as much as the seasonal adjustment assumes it should, so the expansion got transformed into a contraction.

This is not unusual. Retail businesses hire lots of people for the holiday shopping season. The seasonal adjustments try to smooth this out so that it doesn’t look like there’s been an underlying surge of demand for labor when there has just been a seasonal surge. As a result, there’s always a large gap between the unadjusted and adjusted figure for retail trade in November.

This chart shows the gap between seasonally adjusted retail trade employment gains and unadjusted gains. Those spikes are all from Novembers and Decembers.

The economists at the Department of Labor laugh at the focus Wall Street and the financial media put on month-to-month changes in seasonally adjusted figures, whether in inflation or employment. Economist Claudia Sahm‘s famous rule about recessions uses three-month moving averages of unemployment to detect recessions for a similar reason. The one month seasonally adjusted figure contains too much noise.

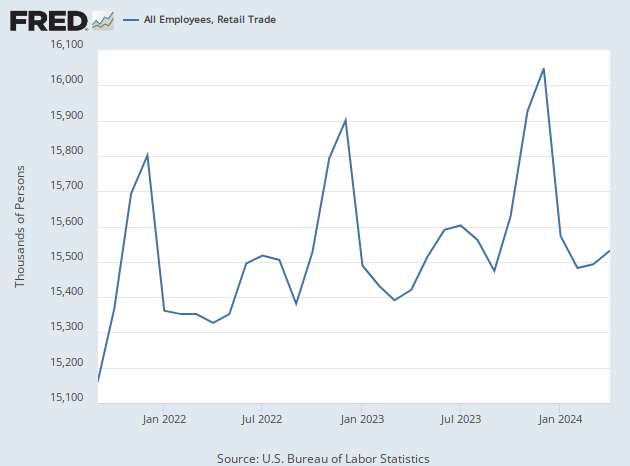

For the purposes of evaluating the strength of the consumer and what that might mean for the economy, it’s probably best to look at the year-over-year chart of the level of retail employment.

As you can see, this November’s retail employment is the highest it has been in the post-pandemic period for the month of November. In fact, we’re just short of last year’s December peak.

One of the reasons November’s month-to-month payrolls gain might not have been as impressive as the seasonal adjustments assume is that October’s figure was also strong. Retailers are responding to consumers doing their shopping early by hiring workers earlier. The seasonal adjustment has not yet caught up to this trend, however, so it reads October as stronger than expected and November as weaker.

Given this stronger than expected gain in employment and solid gain in seasonal retail hiring, it’s no wonder the University of Michigan’s consumer sentiment measure soared so much in early December.

COMMENTS

Please let us know if you're having issues with commenting.