What Do Fed Chairs Maximize?

Thirty years ago the famous Seventh Circuit federal appeals court judge Richard Posner authored a law review article with the provocative title of “What Do Judges and Justices Maximize?” His somewhat unhelpful top line answer was contained right in the subtitle: “The Same Thing Everyone Else Does.”

Posner argued that although the constitution and law had set up various guardrails—lifetime appointments, salaries that could not be reduced or raised above those of their peers, a generous pension system, very limited opportunity for advancement (especially for appellate judges)—that appeared to insulate federal judges from the material concerns faced by the rest of us in our careers, judges are still rational actors in the economic sense. Which is to say, they are still self-interested, they still respond to incentives, and they still seek to maximize the rewards available to them.

Posner sought to find the answer to his question by exploring three roles he considered analogous to judging: non-profit enterprises, voters in public elections, and spectators at theatrical events. To skip to his conclusion, Posner concluded that judges seek to maximize their prestige, reputation, influence, leisure, and enjoyment—although not necessarily in that order. Basically, judges want to be respected by their peers and by the history books while also enjoying their jobs.

Powell’s Choice: Burns or Volcker?

Posner’s approach can be adopted when evaluating what policies Federal Reserve Chairman Jerome Powell is likely to adopt.

Will Powell continue to raise rates? Will he keep rates at their current level or higher even in the face of banking turmoil and an economic downturn? Will he cut rates later this year to prevent the economy from falling into severe distress?

As we’ve noted before, the market is currently pricing in a lot of rate cuts this year. Fed funds futures imply even odds of another hike at the May meeting, which is a change from last week when the futures were implying just a 25 percent chance of a hike. But after that, the futures market implies cut after cut. The December figures imply an 85 percent chance that the Fed’s rate target will be lower than it is right now.

So, what would Powell be maximizing if he were to cut rates as much as the market now appears to expect? We suppose venture capitalists and tech investors would cheer him on. Left-wing lawmakers would applaud the move, although we suspect it is too late for Powell to win anything but the most grudging support from Sen. Elizabeth Warren (D-MA). Even some conservatives who have concluded that the Fed has gone too far too fast in its hikes might applaud him.

Given Powell’s actions last year, however, these do not seem to be big motivating factors for him. We suspect the very tarnished reputations of Fed chairmen Arthur Burns and G. William Miller weigh more heavily on his mind. They are probably best known today for repeatedly prematurely backing off from fighting inflation due to concerns about growth and unemployment. As a result, progress in bringing down inflation stalled three times and then surged to even higher levels.

Federal Reserve Chairman Arthur Burns tells the Congressional Joint Economic Committee that inflation threatens to run rampant, during a hearing on Capitol Hill on July 26, 1972. (Getty Images)

Powell most likely would prefer to be thought of as a new Paul Volcker, now lionized for taming the out-of-control inflation of the 1970s and early 1980s. It’s now largely forgotten, but Volcker was tested to the extreme during his tenure, attacked from both the left and the right. Reagan administration officials accused him of undermining their attempt to marshal supply-side economics to restore non-inflationary economic growth. Volcker’s ability to maintain his stance is now credited with establishing the credibility of the Fed’s independence and its dedication to price stability.

Federal Reserve Chairman Paul Volcker speaks at a Congressional Domestic Policy Subcommittee on Capitol Hill on Nov. 1, 1980. (Diana Walker/Getty Images)

For a central banker seeking to maximize prestige, reputation, and influence, the choice is pretty clear. As for enjoyment and leisure, it’s not clear those are much influenced by the fed funds rate. If Powell is rational—and we suspect that he is—the contrast in reputation and influence will not be lost on him. Which means the market may be disappointed that Powell turns out to be more Volcker than Burns.

Money Supply Points to Higher Inflation for Longer

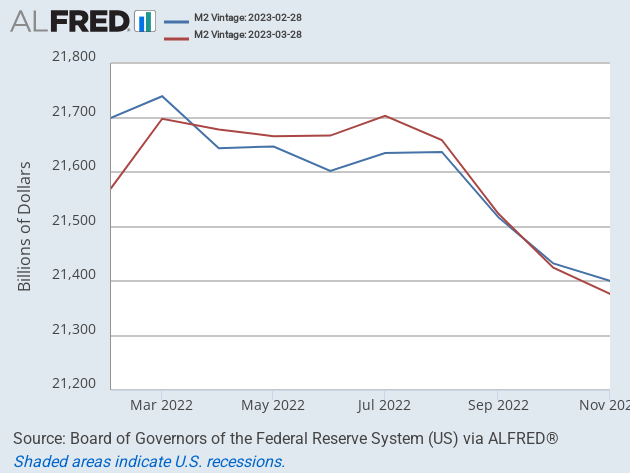

Yesterday, we explained how the March revisions to last year’s M2 money supply created reasons to significantly revise expectations on inflation and economic growth. Specifically, the revised numbers showed that the money supply had been higher than we previously thought through most of last year and that the peak of M2 happened later.

This chart, which we produced with the help of the kind folks at the St. Louis Fed, shows the difference between the “vintage” data reported through February (blue line) and the revised data reported this week (red line).

The lines are pretty close and follow the same trajectory in the second half of the year, but in the spring and summer it is clear that the money supply was higher than was understood. This nicely illustrates that the Fed waited at least one quarter too long to bring down inflation. And it suggests that it will take longer for inflation to come down than expected.

COMMENTS

Please let us know if you're having issues with commenting.