Critics of Donald Trump’s tax proposal are getting increasingly desperate, resorting to obvious falsehoods to bolster their case against tax cuts.

Steve Rattner, probably best known these days as a frequent guest on MSNBC’s Morning Joe, recently wrote an Op-Ed for the New York Times warning that Trump’s tax cut proposal would have dire consequences for the fiscal health of the United States government. The only parts of it that aren’t merely misleading are those riddled with errors and falsehoods.

Matthew Klein, of the Financial Times’ blog FT Alphaville, has a devastating analysis of Rattner’s Op-Ed. It’s necessary to quote it at length in order to convey the sense of how thoroughly and brutally Klein tears apart Rattner’s mendacious argument. Of course, you should read the entire article at FT Alphaville.

President Donald Trump wants to cut taxes. Reasonable people can disagree whether this is a good idea and can also disagree on the merits of the specific priorities reiterated last week.

But reasonable people also need to support their arguments with actual substance rather than platitudinous scare-mongering — especially when their argument includes dire warnings against the long-term consequences for the budget deficit. A recent article by former “car czar” and disgraced private equity investor Steven Rattner fails the test.

Rattner worries that “huge, unpaid-for tax reductions that saddle us with large amounts of new debt” will burden “our children and grandchildren”. Rattner’s main piece of evidence is the 1981 tax cut, which he claims “increased the budget deficit, helping elevate interest rates over 20 percent, which in turn contributed to the double-dip recession that ensued”.

Literally none of that is true.

Klein points out that the Reagan tax cuts did not have a significant effect on the budget deficits. What really drove up deficits were spending increases, which were largely a result of a rise in unemployment from 6 percent in 1979 to nearly 11 percent in 1981. That rise in unemployment was due to a recession triggered byPaul Volcker’s decision to raise interest rates dramatically in an attempt to crush inflation “by any means necessary.”

The downturn hit tax revenues since fewer people working means less income to tax. In addition to the tax hit, there was a lot more spending on jobless benefits and other programmes meant to help the needy. Unsurprisingly, the federal government budget deficit widened from about 2 per cent of gross domestic product in 1979 to roughly 7 per cent by mid-1983.

This is a general pattern. For more than six decades, changes in America’s federal government budget balance are almost perfectly inverted with changes in the jobless rate:

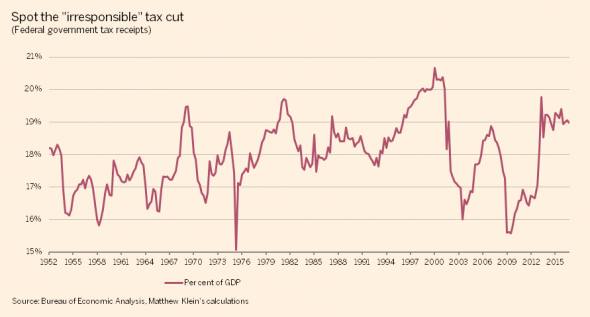

Contrary to Rattner’s narrative, almost the entire change in the budget balance in the early 1980s can be explained by higher spending, not lower taxation. Federal tax receipts were 18.7 per cent of GDP in 1979. By mid-1983, when the budget deficit had reached its peak, that number had dropped to…18.3 per cent:

So much for the idea that Reagan’s tax cuts caused budget deficit’s to soar.

What about interest rates and the recession? Klein points out that Rattner’s claim that deficits caused interest rates to rise or contributed to the recession is also one hundred percent bunk.

It should be obvious that the spike in interest rates in the early 1980s and the depth of the downturn are attributable to Volcker’s determination to squash inflation, rather than anything to do with tax policy, but it’s worth reiterating because Rattner’s claim that the 1981 tax cuts “contributed to the double-dip recession” is utter nonsense.

The chart below shows the effective interest rate paid by the federal government on its debt:

If the budget balance mattered for interest rates, the implication would be that America suffered from decades of ever-worsening profligacy since the early 1950s until things turned around in the early 1980s. One might also notice that almost the entire decline in the government’s effective borrowing cost in the past 35 years occurred under fiscally “irresponsible” Republican presidents.

Of course, the budget balance doesn’t affect interest rates, except insofar as it affects inflation and growth.

Finally, Klein refutes Rattner’s irresponsible scare-mongering about Trump’s tax cuts saddling future generations with debt.

So Rattner is fundamentally wrong about what happened in the early 1980s. That should be enough to discard the rest of his piece, which also frequently features the classic charlatan move of citing debt and deficit figures in absolute terms. No one should care how big the national debt is now compared to the days when bell-bottoms were considered fashionable.

But there is one other important error that needs to be addressed: Rattner’s claim that “large fiscal gaps simply mean more debt that will be left to our children and grandchildren to pay off”.

Government debt isn’t supposed to be paid off! People buy sovereign bonds because they want to store wealth in something that does well when the rest of the economy does badly. One of the central problems of the past few decades has been the stubborn refusal of certain governments, including America’s, to accommodate this desire, suppressing real interest rates and encouraging the unscrupulous to create imperfect substitutes for safe debt. Rattner doesn’t seem to think banks should “pay off” their deposit obligations and liquidate themselves. So why should the government?

It’s worth keeping in mind that this is not coming from a bastion of pro-Trump conservative thinking. This is FT Alphaville, the highly respected news and commentary site for financial professionals. So Klein’s critique cannot be dismissed as partisan attack on Rattner.

Rattner’s Op-Ed, like much of the deficit fear-mongering that has suddenly emerged on the left, is just too far removed from reality for even disinterested market watchers to accept.

COMMENTS

Please let us know if you're having issues with commenting.

COMMENTS

Please let us know if you're having issues with commenting.